Chapter 23 — Monetary Policy

Cambridge International AS & A Level Economics (9708) · Unit 5.3 · 4th edition coursebook

Learning objectives

- Define the meaning of monetary policy.

- Explain the main tools of monetary policy, including interest rates, the money supply, credit regulations.

- Explain the difference between expansionary and contractionary monetary policy.

- Discuss, using AD/AS analysis, the impact of expansionary and contractionary monetary policy on equilibrium level of national income, the real level of output, the price level and employment.

Key terms

- central bank

- Bank owned by the government that provides banking services to the government and commercial banks and which operates monetary policy.

- commercial banks

- Banks which aim to make a profit by providing a range of services to firms and households.

- monetary policy

- The use of interest rates, the money supply, credit regulations and the exchange rate to influence aggregate demand.

- interest rates

- The price of borrowing money and the reward for saving.

- money supply

- The total amount of money in a country.

- target rate for inflation

- The rate a central bank is set to achieve.

23.1What is monetary policy?

Monetary policy refers to any policy tools that affect the price or quantity of money. Like fiscal policy, monetary policy is a demand-side policy: it seeks to influence aggregate demand. Monetary policy tools are usually applied by the country's central bank. Monetary policy has traditionally been used to achieve price stability. More recently, the governments of a number of countries have also begun to use monetary policy to encourage economic growth, particularly during and after recessions when interest-rate cuts alone were judged insufficient to lift demand.

Expansionary monetary policy aims to stimulate AD by making money cheaper and more plentiful. The central bank therefore lowers interest rates and/or increases the money supply. Tightening credit regulations or raising the interest rate would be contractionary; raising the exchange rate would also dampen AD by reducing net exports. Increasing the money supply is the textbook expansionary monetary action.

23.2The tools of monetary policy

The main tools of monetary policy are interest rates, the money supply, the exchange rate, and credit regulations.

Interest rates

In recent years, changes in interest rates have been the main monetary policy tool used by central banks to control inflation and influence economic activity. The interest rate is, in effect, the price of money. Households and firms that borrow money have to pay interest; those who lend money are paid interest. The interest rate charged by the central bank may be called the bank rate, base rate, repo rate, or simply the interest rate. Commercial banks tend to align their own rates with the central bank's rate, because the central-bank rate is what they would pay if they had to borrow from the central bank.

The money supply

A central bank may also target the money supply in the economy, because changes in the quantity of money can influence aggregate demand. A central bank can create money electronically, but the main cause of changes in the money supply in most economies is lending by commercial banks. For this reason, central banks often seek to influence commercial bank lending rather than print money directly.

Exchange rate

Most economists also include the exchange rate among the tools of monetary policy. Central banks may manipulate the exchange rate to raise or lower aggregate demand, and so influence objectives such as price stability. Exchange-rate policy is covered in more depth in Chapter 28.

Credit regulations

Central banks may also impose credit regulations on commercial banks to help maintain financial stability and to influence bank lending. Most central banks require commercial banks to hold a proportion of their assets in a form that can be quickly sold and converted into cash. This ensures that commercial banks can meet their customers' likely demand for cash even during a financial crisis.

Key concept link — Regulation, equality and equity

Regulation of bank lending can be used to protect bank customers and to influence aggregate demand.

23.3The difference between expansionary and contractionary monetary policy

Monetary policy can be either expansionary or contractionary, depending on whether the central bank wishes to raise or restrain aggregate demand. The same set of tools is used in either direction; what differs is which way they are moved.

Expansionary monetary policy is used to increase aggregate demand. A cut in the rate of interest reduces the cost of borrowing for households and firms and reduces the reward for saving, so consumer expenditure and investment are encouraged. An increase in the money supply gives households and firms greater liquidity to spend or to lend, and tends to put downward pressure on interest rates in financial markets. A reduction in any restrictions on bank lending — for example, lower required reserve ratios or looser credit rules — allows commercial banks to make more loans, again expanding spending in the economy. Each of these measures contributes to a rise in aggregate demand, raising real output and employment when the economy has spare capacity.

Contractionary monetary policy is used to reduce aggregate demand, or the growth of aggregate demand, when there is excess demand or inflationary pressure. It may involve a rise in the rate of interest, which makes borrowing more expensive and saving more attractive, dampening consumer expenditure and investment. It may involve a decrease in the money supply, which tightens financial conditions and tends to raise market interest rates. It may also involve tightening restrictions on bank lending, so that commercial banks make fewer loans. The result is to reduce aggregate demand and so to ease inflationary pressure.

In choosing the appropriate stance, the central bank weighs current and forecast economic conditions against its policy objectives — most commonly the inflation target, but also the level of output, employment and the exchange rate.

Key concept link — Equilibrium and disequilibrium / Efficiency and inefficiency

Monetary policy can be used to move the economy from the current macroeconomic equilibrium to a more efficient equilibrium.

A global recession requires an expansionary monetary stance to lift AD. Keeping the rate of interest very low and increasing the money supply directly lowers the cost of borrowing and raises liquidity for spending and investment. Raising business taxation, running a budget surplus or restricting the money supply would all be contractionary and deepen the recession.

23.4The impact of expansionary and contractionary monetary policy

Monetary policy is mainly used to influence the price level. The likely effects on output, the price level and employment depend on the initial level of economic activity, so this should always be considered when discussing the impact of a policy change.

Monetary policy and the price level

In many countries, the main policy used to reduce demand-pull inflation is monetary policy, with the focus on the interest rate. Many central banks are now given a target rate for inflation and instructed to use interest-rate changes to achieve it. If the inflation rate is rising outside its target range, a central bank is likely to raise the rate of interest to reduce aggregate demand. The cost of borrowing rises, discouraging large-scale purchases such as houses and cars. Saving is encouraged because the return from saving rises; the opportunity cost of saving is spending.

Monetarists argue that the only way to reduce inflationary pressure is to lower the growth of the money supply. If increases in the money supply do not exceed increases in output, they suggest, there will be no upward movement of the price level.

A rise in the rate of interest may not always discourage consumer expenditure. Although commercial banks usually keep their rates in line with the central bank's, there is no guarantee that they will always raise their rates when the central bank does. Even when consumers face higher rates, they may not reduce their spending if they are optimistic about the future. A rise in interest rates may also have an adverse effect on investment, because it raises the cost of borrowing funds to invest and raises the opportunity cost of using profits to invest. If investment falls below depreciation, the capital stock will decline, and the resulting fall in aggregate supply can itself push the price level up.

Some countries face constraints on the monetary policy measures they can use to correct inflation. Central banks may be worried that raising interest rates above those in other countries will attract an inflow of money from abroad, which can raise the exchange rate. Countries that are members of an economic union may operate the same interest rate and exchange rate as other members, with the area's central bank taking the relevant decisions.

A government will not seek to stop good deflation but it will try to correct bad deflation. Expansionary monetary policy may be used to try to reverse a fall in aggregate demand. A cut in the interest rate or an increase in the money supply may not be effective, however, because firms and households may be pessimistic during periods of deflation and may not spend more even if money is more plentiful and borrowing is cheaper. When interest rates are already low, it may also not be possible to cut them much further, and any further cuts may have little additional effect. Central banks may expand the money supply, giving commercial banks more funds to lend, but the banks may be reluctant to lend if they think there are few creditworthy borrowers.

Monetary policy and equilibrium national income, real output and employment

If there is spare capacity in the economy, an expansionary monetary policy can raise national income. A cut in the rate of interest or an increase in the money supply can encourage more consumer expenditure and investment. The higher aggregate demand shifts the AD curve to the right and raises real output (see Figure 23.5). Higher output is likely to result in an increase in employment, as extra workers are taken on to produce more goods and services.

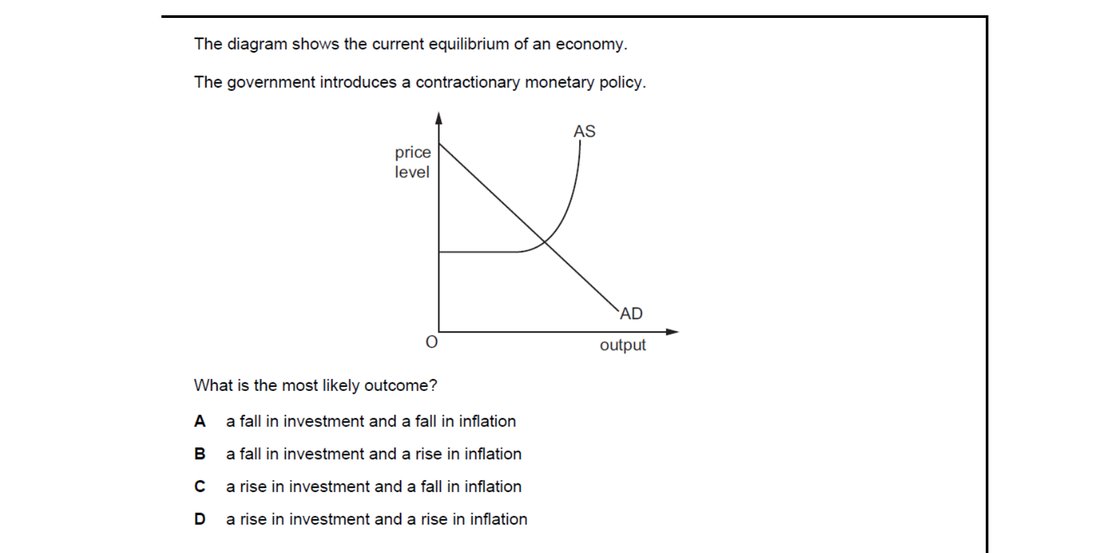

There is a risk that contractionary monetary policy may reduce national income, output and employment. However, if it is used when the economy is operating with all resources employed, it may reduce the inflation rate. Without the downward pressure on the growth of consumer expenditure and investment, the price level would rise further than it does once contractionary policy is applied (see Figure 23.6).

The effectiveness of monetary policy

In practice it can be difficult to control the money supply. Commercial banks have a strong incentive to try to increase their lending and may seek to get round any limits the central bank places on the growth of their lending. Trying to control certain forms of money may also lead to new forms of money being used.

Using interest rates is also not without problems. There is a time lag between changing interest rates and the full effect being transmitted to the macroeconomy. Some economists have estimated that it can take as long as 18 months for interest-rate changes to have their full impact, although this is still shorter than the lag for some fiscal policy measures.

Interest-rate changes are a powerful policy measure but also a blunt and uncertain one. Some households and firms cope better than others with a change in the interest rate. A rise harms borrowers but benefits savers. A higher rate may also have an adverse effect on unemployment and economic growth, as with a deflationary fiscal policy measure. With increasing mobility of financial investment, it can also be difficult for a country to operate an interest rate that is significantly different from that of rival countries.

Raising interest rates curbs spending by making borrowing dearer and saving more attractive. But if consumers expect even faster price rises ahead, they have a strong incentive to buy now before prices climb, dampening the response of spending to higher rates. Inflationary expectations therefore blunt the effectiveness of a rate rise as an anti-inflation tool.

Contractionary monetary policy raises interest rates and/or reduces the money supply. Higher borrowing costs make firms postpone or cancel investment projects, so investment falls. The leftward shift in AD reduces inflationary pressure, so the price level rises more slowly — inflation falls. The pairing of falling investment with falling inflation is therefore the expected outcome.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

A deflationary downturn calls for a fast boost to AD. Helping banks lend more increases credit creation immediately, raising consumer spending and investment quickly. Raising the budget surplus is contractionary; long-term transport investment has long implementation lags; switching taxation from income to spending is a structural fiscal reform, not an immediate stimulus. Easing bank lending acts the fastest.

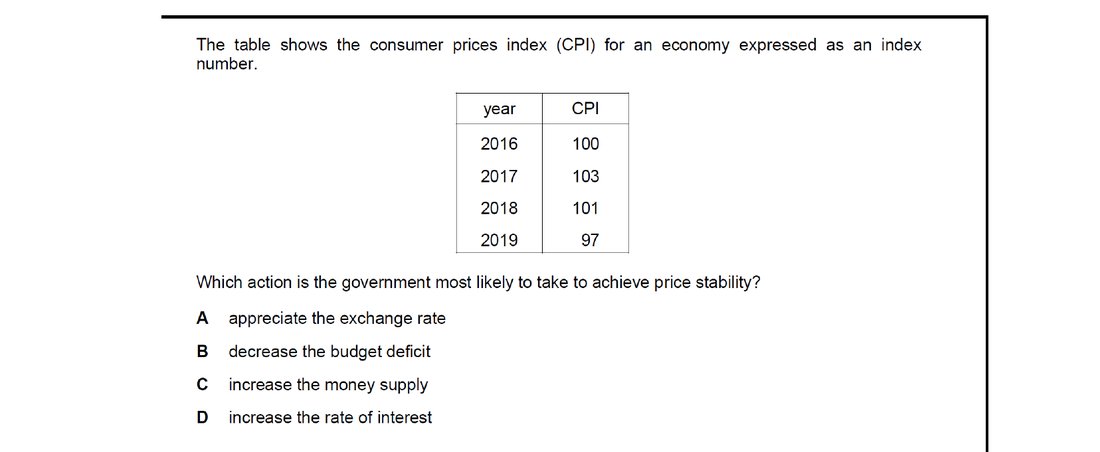

The CPI series falls from 103 to 101 to 97 — the economy is experiencing deflation, not inflation. To restore price stability, the government wants to push AD up and lift the price level back to a steady positive growth path. Increasing the money supply (expansionary monetary policy) is the appropriate response; appreciating the currency, cutting the budget deficit or raising the interest rate would all worsen deflation.

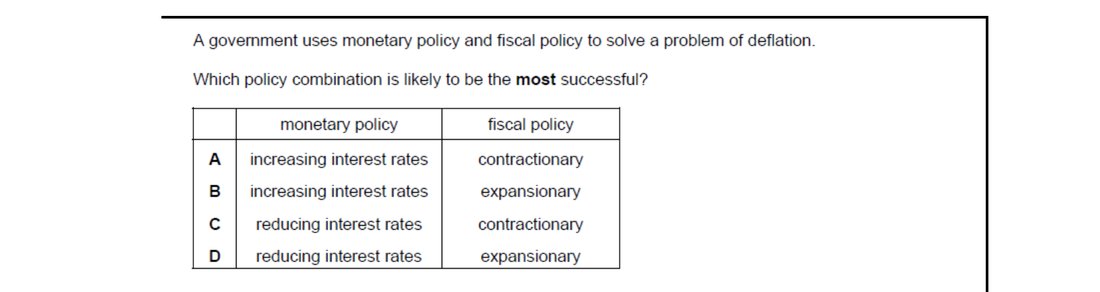

Deflation reflects deficient AD, so both arms of policy should be expansionary. Reducing interest rates is expansionary monetary policy, and expansionary fiscal policy (higher G or lower taxes) directly raises AD. Combining the two delivers the strongest, fastest stimulus and is the most likely to bring inflation back to a positive, stable rate.

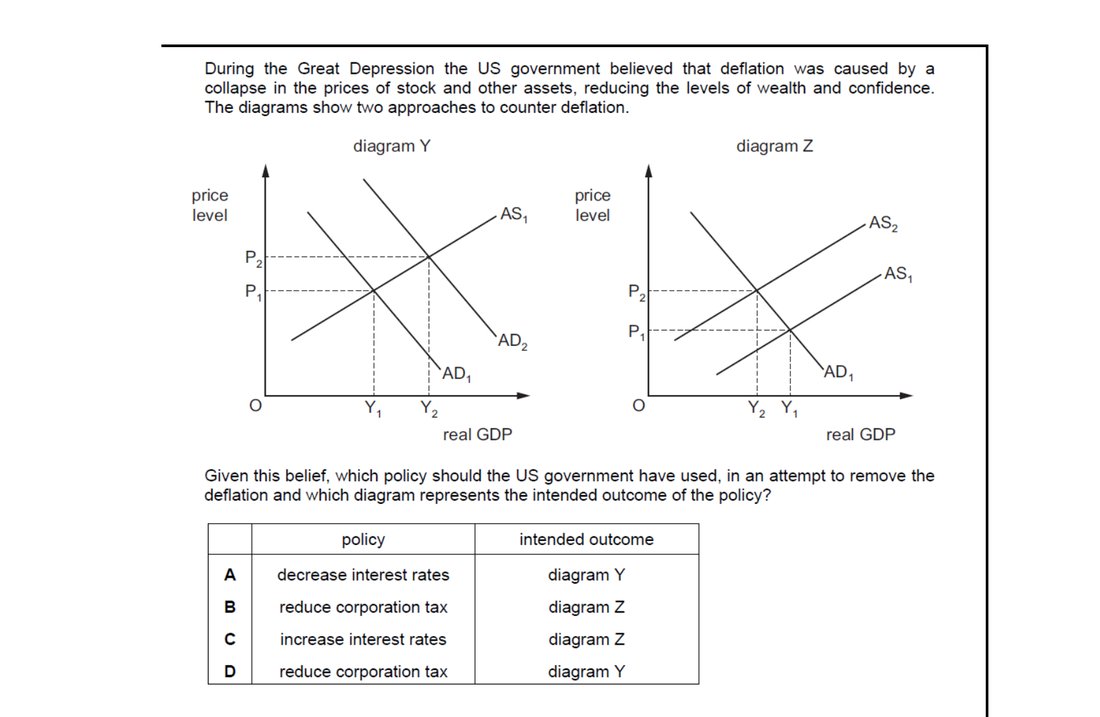

If the cause is a collapse in asset prices, wealth and confidence — i.e. a fall in AD — the right response is expansionary monetary policy, which is decreasing interest rates. The intended outcome is a rightward shift of AD, raising both the price level and real output, which is precisely what diagram Y depicts. Reducing corporation tax is fiscal, not monetary, and raising rates would worsen the deflation.

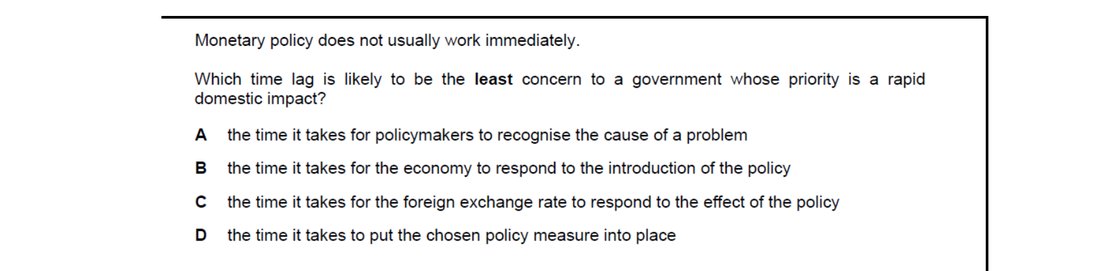

For a government focused on a rapid domestic impact, lags that delay the policy's effect on home spending and prices are critical: recognition lag, implementation lag and transmission to the real economy. The time the foreign exchange rate takes to respond matters only for the external channel; if the priority is domestic, this lag is the least pressing concern.

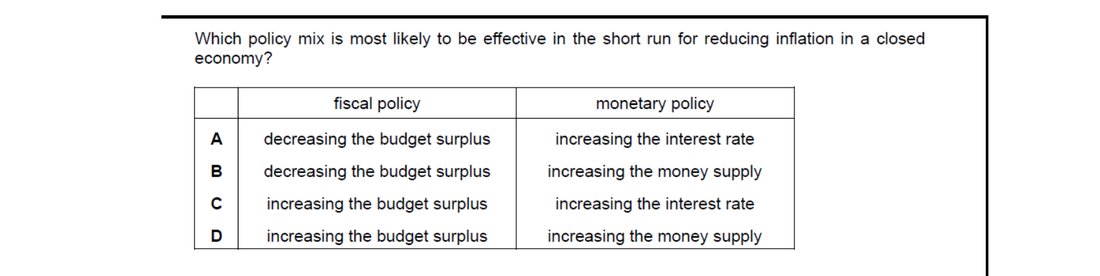

Reducing inflation requires lowering AD. The combination of an increased budget surplus (contractionary fiscal policy: less government spending or higher taxes) and a higher interest rate (contractionary monetary policy) reinforces each other, cutting both private and public spending. The other combinations include at least one expansionary measure and so are weaker or contradictory.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Understand that monetary policy seeks to influence aggregate demand (AD) by affecting the price and quantity of money.

- Explain the main tools of monetary policy: interest rates, money supply, credit regulations.

- Differentiate between expansionary monetary policy that aims to increase AD and contractionary monetary policy that aims to reduce AD or the growth of AD.

- Use AD/AS analysis to consider the impact of expansionary and contractionary monetary policy on equilibrium national income, real output, the price level and employment.

Want more practice? Drill this chapter's past-paper MCQs (65 questions) →